Getting Ready for the Start of Trump Accounts in July 2026 – Serving Those Who Serve

![]()

Trump accounts are a new type of custodial-style traditional IRA for minor children. The accounts are owned by a child but administered by an adult. They are set to launch on July 4,2026 under provisions of the One Big Beautiful Bill Act (OBBBA) of 2025. This column presents information on Trump Accounts including how they work, who can contribute, and how they can be invested.

What is a Trump Account?

A Trump Account is a traditional IRA established for a child under age 18. According to IRS guidance, a Trump Account is designated as a traditional IRA at the time of opening. The child for whom the account is opened is the beneficiary and the legal owner of the account. Trump accounts are designed to help families start saving and investing for a child’s future when the child is young. This is done through the use of a familiar retirement account framework. Trump Accounts are administered by the US Treasury Department.

Eligibility for a Trump Account

Children under age 18 with a Social Security number are eligible for a Trump Account. The US Treasury’s pilot program adds a one-time $1,000 “seed” contribution for US citizens born between January 1,2025 and December 31, 2028. Only one funded Trump Account is allowed per eligible child.

How a Trump Account Works

Trump accounts work much like a custodial IRA, but with special rules for contributions, investments and withdrawals. Family members can fund the account through individual contributions and through employer programs that allow both employee and employer contributions. Details of individual and employer-sponsored program contributions are discussed below.

Trump Account Contributions

The maximum contribution that can be made to a Trump Account is $5,000 per year. Multiple sources can contribute each year. Contribution limits apply across all sources with one exception. The federal government “seed” contribution amount of $1,000 and qualified general contributions from charitable organization do not count toward the yearly $5,000 limit. These exceptions can make a major difference for eligible families. The following offers the details of who can contribute to a Trump Account on behalf of a child under age 18.

It is important for potential Trump Account investors to understand that contribution sources will determine how future taxes will apply to distributions. Investors are therefore advised to keep accurate records of contribution sources and amounts. Regardless of contribution sources, all Trump Account earnings, when distributed, will be fully taxable.

Trump Account Withdrawals

Potential Trump Account investors are advised that Trump Accounts are designed for long-term savings. The means that withdrawals are highly restricted before the account owner (the child) becomes aged 18. Before the account owner becomes aged 18, account withdrawals are generally not allowed except for limited rollovers.

When a Trump Account beneficiary (that is, the child who is the Trump Account owner) reaches age 18, the beneficiary has three options for the account. The three options are:

Trump Accounts that are left alone when a child becomes age 18 will potentially grow tax-deferred and be penalty-free of federal and state income taxes until the child becomes age 59.5. At that time, the child can make penalty-free withdrawals but must pay federal and state income tax on the taxable portion of the account.

Trump Account Investment Options

Investment options for Trump Accounts are the following types with certain features:

How to Open a Trump Account

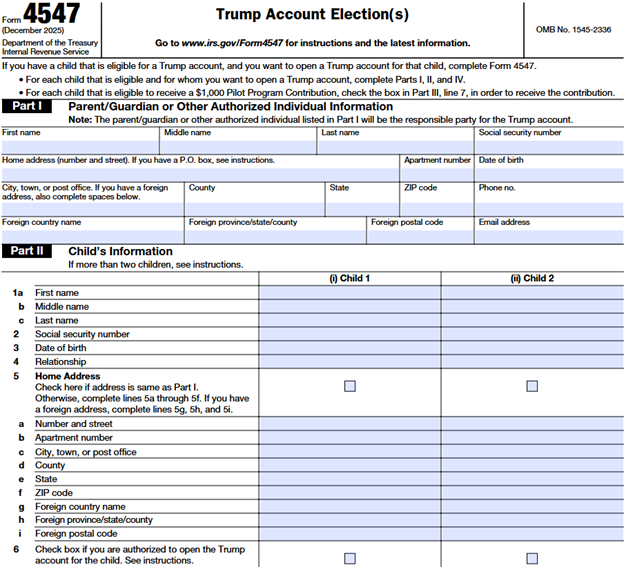

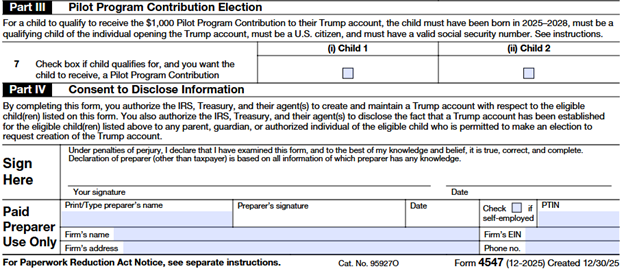

Parents who want to open a Trump Account will need to do so with an election process through the IRS either by filing IRS Form 4547 (Trump Account Election) (see below for a draft version of IRS Form 4547) or using an upcoming online tool at Trumpaccounts.gov. Trump Account elections are scheduled to start in mid-2026, with accounts becoming available July 5, 2026. Once the election is complete, the US Treasury will provide instructions to activate the account.

The IRS is expected to issue more guidance for rollover accounts at financial institutions. This can only happen after the initial Treasury account exists. These details will be clarified and provided as the Trump Account program expends.

Edward A. Zurndorfer is a CERTIFIED FINANCIAL PLANNER™ professional, Chartered Life Underwriter, Chartered Financial Consultant, Chartered Federal Employee Benefits Consultant, Certified Employees Benefits Specialist and IRS Enrolled Agent in Silver Spring, MD. Tax planning, Federal employee benefits, retirement and insurance consulting services offered through EZ Accounting and Financial Services, and EZ Federal Benefits Seminars, located at 833 Bromley Street – Suite A, Silver Spring, MD 20902-3019 and telephone number 301-681-1652. Raymond James is not affiliated with and does not endorse the opinions or services of Edward A. Zurndorfer or EZ Accounting and Financial Services. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional.

© 2025. All Rights Reserved.

15245 Shady Grove Rd Ste 240

Rockville MD 20850-3239

Phone 301-216-1111

Lee Sipe and Associates DBA Serving Those Who Serve.

2025 Forbes Best-in-State Wealth Management Teams

Best-In-StateWealth Management Teamsis based on an algorithm of qualitative criteria, mostly gained through telephone and in-person due diligence interviews, and quantitative data. This ranking is based is based on an algorithm of qualitative criteria, mostly gained through telephone and in-person due diligence interviews, and quantitative data. This ranking is based upon the period from 6/30/2023 to 6/30/2024 and was released on 4/8/2025. Those advisors that are considered have a minimum of seven years of experience, and the algorithm weighs factors like revenue trends, assets under management, compliance records, industry experience and those that encompass best practices in their practices and approach to working with clients. Portfolio performance is not a criteria due to varying client objectives and lack of audited data. Out of approximately 48,944 nominations, roughly 9,722 advisors received the award. This ranking is not indicative of an advisor’s future performance, is not an endorsement, and may not be representative of individual clients’ experience. Neither Raymond James nor any of its Financial Advisors or RIA firms pay a fee in exchange for this award/rating. Compensation provided for using the rating. Raymond James is not affiliated with Forbes or Shook Research, LLC.

Please see https://www.forbes.com/lists/wealth-management-teams-best-in-state/ for more info.

Securities offered through Raymond James Financial Services, Inc., member FINRA/SIPC, marketed as Serving Those Who Serve (STWS). Investment advisory services offered through Raymond James Financial Services Advisors, Inc. Serving Those Who Serve (STWS) is separately owned and operated and not independently registered as a broker-dealer or investment adviser. Raymond James financial advisors may only conduct business with residents of the states and/or jurisdictions for which they are properly registered. Therefore, response to a request for information may be delayed. Please note that not all of the investments and services mentioned are available in every state. Investors outside of the United States are subject to securities and tax regulations within their applicable jurisdictions that are not addressed on this site. Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website’s users and/or members. Contact our office for information and availability.

Raymond James Legal Disclosures including Form CRS

Raymond James Privacy Policy

Check the background of this firm on FINRA’s BrokerCheck

Finra

SIPC

STWS is owned and operated by Daniel Sipe and Tom Lee (the “Financial Advisors”). The Financial Advisors are registered financial professionals of Raymond James Financial Services, Inc. (“RJFS”), a broker-dealer registered with the Securities and Exchange Commission (“SEC”), and Raymond James Financial Services Advisors, Inc. (“RJFSA”), an investment adviser registered with the SEC, (collectively, with their affiliates, “Raymond James”).

Mr. Zurndorfer does not pay compensation to or receive compensation from STWS in connection with Presentations hosted by Mr. Zurndorfer. However, Mr. Zurndorfer does provide similar educational presentations at certain Federal Retirement Benefits Seminars (“Seminars”) hosted by STWS, for which Mr. Zurndorfer receives compensation from STWS. All presentations, seminars, articles and videos are informational in nature and are not geared toward the circumstances or goals of any particular attendee; they are not intended to be, and should not be relied upon as, investment advice to anyone or a solicitation of Raymond James’ services.

Mr. Zurndorfer is not affiliated with Raymond James, and is not authorized to provide investment advice on behalf of Raymond James, to solicit or refer investors to Raymond James, or to act for or bind Raymond James. The presentations, seminars, articles, videos, Mr. Zurndorfer, and the educational information provided therein are not sponsored or endorsed by Raymond James, and should in no way be considered an endorsement of, referral to, recommendation for, or offer to purchase any product or service from Raymond James or the Financial Advisors.

Federal government agencies, including the SEC, do not endorse or sponsor particular securities, issuers, products, services, professional credentials, firms, or individuals. Neither Raymond James, the Financial Advisors, STWS, nor Mr. Zurndorfer are affiliated with, endorsed by, or authorized to speak on behalf of the U.S. Government, the Federal Employee Retirement System, or any other Federal Government-sponsored benefits programs or retirement plans, including the Thrift Savings Plan (collectively, “Federal Benefits Plans”).